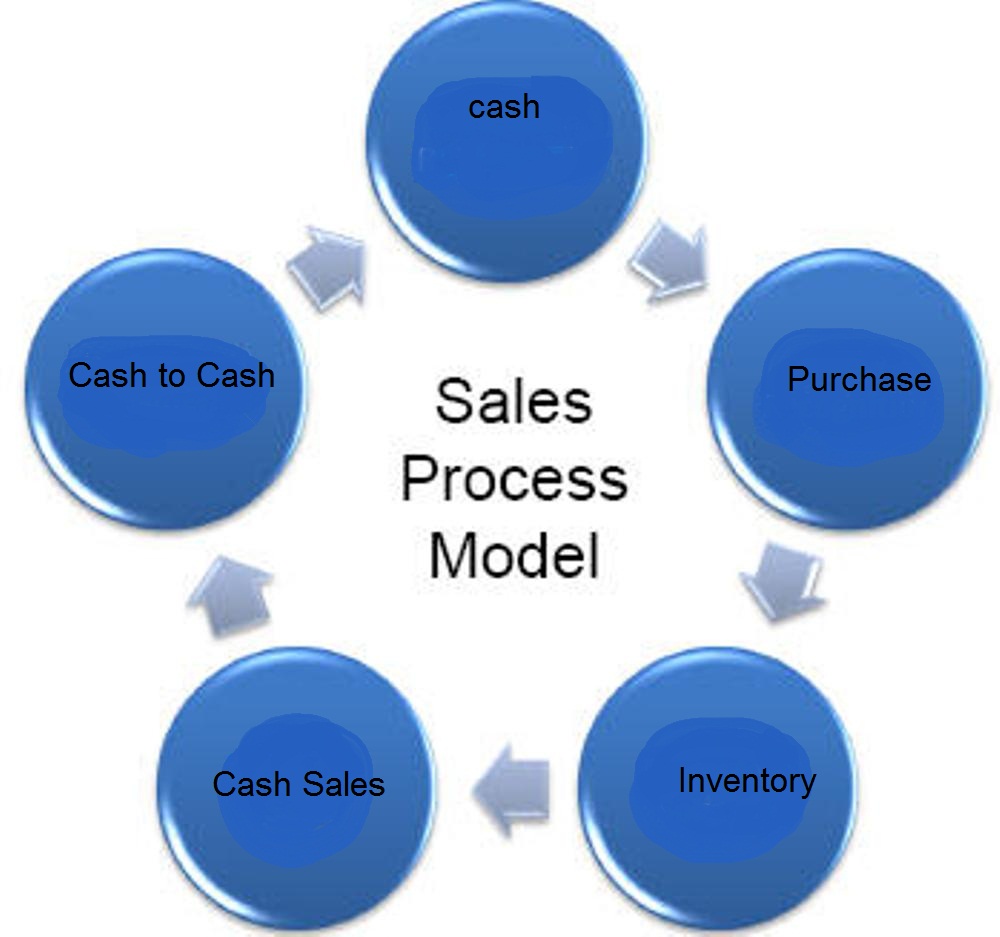

The merchandising entity purchases inventory , sells the inventory and uses the cash to purchase more inventory- and cycle continues. For Cash Sales, the cycle is from cash to inventory and back to cash. For sales on account, the cycle is from cash to inventory to accounts receivable and back to cash. In any industry, manager strives shorten the cycle. The faster sale of inventory and the collection of cash, the higher the profits. The following illustration the operating of a merchandising company.

{kind=link}

Sales on Account Cash Sales

Sales on Account

Merchandise inventory is goods that have been acquired by a distributor, wholesaler, or retailer from suppliers, with the intent of selling the goods to third parties.

ReplyDeleteThis can be the single largest asset on the balance sheet of some types of businesses.

If these goods are sold during an accounting period, then their cost is charged to the cost of goods sold, and appears as an expense in the income statement in the period when the sale occurred.

If these goods are not sold during an accounting period, then their cost is recorded as a current asset, and appears in the balance sheet until such time as they are sold.